How Inflation Is Stealing Our Money

Inflation is often described in dry economic terms—percentages, indexes, and monetary policies. But for everyday people, inflation feels like something much more tangible: it’s the slow and steady disappearance of our purchasing power. It’s the reason your grocery bill is higher this month than it was last year. It’s why your paycheck doesn’t go as far, your savings feel weaker, and your plans for the future seem more expensive. Inflation, in many ways, is silently stealing our money—and unless we understand how, we’re left vulnerable to its effects.

What Is Inflation, Really?

At its core, inflation is the rate at which the general level of prices for goods and services rises, eroding the purchasing power of currency. When inflation occurs, each unit of currency buys fewer goods and services. Over time, this means that unless your income increases at the same rate—or faster—you’ll be able to afford less.

A simple example: if the annual inflation rate is 5%, something that costs $100 today will cost $105 next year. If your salary doesn’t increase to match, you’re effectively poorer.

There are several types of inflation—demand-pull, cost-push, and built-in inflation—but the outcome is the same: prices go up, and your money buys less.

The Real-World Effects

Inflation affects nearly every aspect of our daily lives:

1. Groceries and Essentials

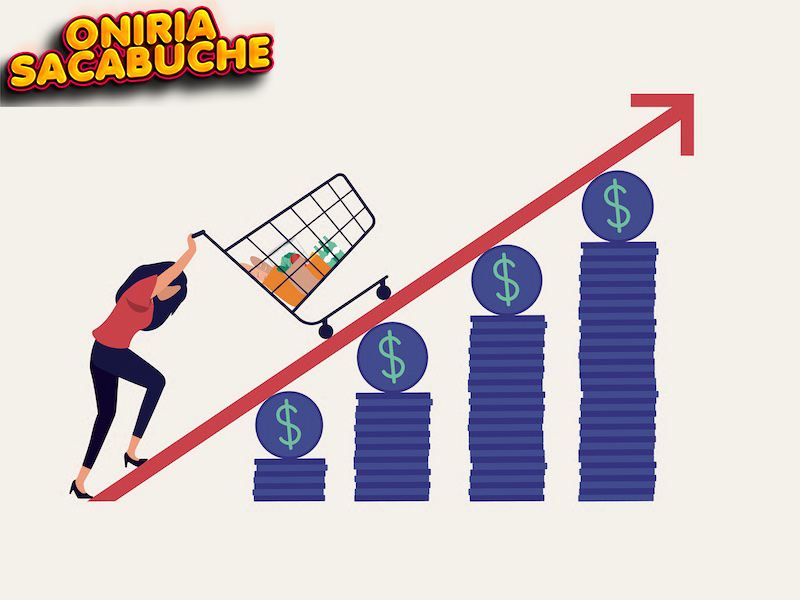

You probably don’t need an economist to tell you that the cost of groceries has gone up. Food prices are among the most noticeable indicators of inflation, as they’re items we buy regularly. From eggs and milk to bread and meat, many of us have noticed that what once filled our cart for $100 now barely covers the essentials.

2. Housing and Rent

For renters and homeowners alike, inflation hits hard. Housing prices have surged in many regions, and rent continues to climb. Even mortgage payments can become more burdensome if inflation drives up interest rates. Landlords often increase rent to match inflation, passing the cost onto tenants.

3. Savings and Retirement

One of the most insidious ways inflation steals money is by eroding savings. If your money is sitting in a bank account earning 1% interest while inflation is running at 4%, you’re losing 3% of your purchasing power every year. Over time, this compounds into a significant loss. Retirement plans based on fixed incomes can also suffer, as the cost of living rises while income remains stagnant.

4. Wages and Salaries

While wages do tend to rise over time, they often lag behind inflation. If your salary increases by 3% but inflation is at 5%, you’re effectively making less money. This wage stagnation hits especially hard for workers on fixed or minimum incomes, widening the gap between the rich and the poor.

Why Inflation Happens

Inflation isn’t necessarily a bad thing—in moderation. Economists often target a 2% inflation rate as a healthy sign of a growing economy. But when inflation runs high and becomes unpredictable, it creates uncertainty and financial hardship.

Several factors can cause inflation:

-

Increased demand: When demand outpaces supply, prices go up.

-

Supply chain issues: Disruptions (like those during the COVID-19 pandemic) reduce supply, increasing costs.

-

Rising production costs: If the cost of raw materials, energy, or labor goes up, businesses pass those costs to consumers.

-

Government policies: Excessive money printing, stimulus packages, and low interest rates can all contribute to inflation by injecting too much money into the economy.

Who’s to Blame?

It’s easy to point fingers—at governments, central banks, corporations—but the truth is more complicated. Inflation often results from a complex mix of global and local factors. That said, policy decisions play a significant role.

When central banks keep interest rates too low for too long or inject large amounts of money into the economy without corresponding growth in production, inflation can surge. Additionally, poor regulation, excessive government spending, and supply chain mismanagement can all worsen the situation.

Some argue that corporations use inflation as a cover for increasing prices beyond their actual cost increases, boosting profits while blaming “inflation” for the hikes. Whether that’s true or not, the result is the same: consumers pay more.

What Can You Do About It?

You can’t control inflation—but you can take steps to protect yourself from its effects.

1. Invest Wisely

Money sitting in a savings account loses value over time. Investing in assets that historically outpace inflation—like stocks, real estate, or inflation-protected securities—can help preserve and grow your wealth.

2. Diversify Your Income

Relying on a single income stream can be risky. Exploring side hustles, freelance opportunities, or passive income sources can provide financial cushioning.

3. Cut Unnecessary Expenses

While it’s not a fun solution, trimming non-essential expenses helps stretch your money further during inflationary periods.

4. Negotiate for Raises

Don’t be afraid to ask for raises that reflect the cost of living. Employers often expect these discussions and may be willing to adjust compensation to retain talent.

5. Stay Informed

Understanding economic trends and inflation’s causes can help you make smarter financial decisions. Knowledge is power—and in times of economic uncertainty, it’s your best weapon.

The Psychological Toll

Beyond the numbers, inflation also takes a mental and emotional toll. It creates anxiety about the future, resentment over wage stagnation, and frustration with a system that seems to reward the wealthy while everyone else falls behind.

When inflation rises, people feel like they’re working harder for less. It can lead to a loss of trust in institutions, in markets, and even in the value of money itself. This psychological impact can be as damaging as the financial one, leading to pessimism, reduced spending, and economic slowdown—a vicious cycle.

Conclusion: Inflation as a Silent Thief

Inflation doesn’t steal your money in one dramatic swoop. It doesn’t empty your bank account overnight. Instead, it quietly erodes your purchasing power over months and years. It’s a slow leak in your wallet, a thief that slips in unnoticed until you suddenly realize you can no longer afford the life you once had.

But you’re not powerless. By staying informed, making smart financial choices, and advocating for fair economic policies, you can protect yourself and your future. Inflation may be an inevitable part of modern economies—but with the right tools, you can fight back against the silent theft it represents.